It is a type of continuous probability distribution for a random variable. It is also called as Normal distribution.

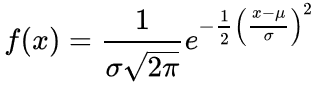

The general form of its probability density function is;

Here the parameter µ is the mean or expectation of the distribution and σ is the standard deviation.

When the mean becomes 0 and variance becomes 1 in a Gaussian distribution, it becomes a Standard Normal Distribution.

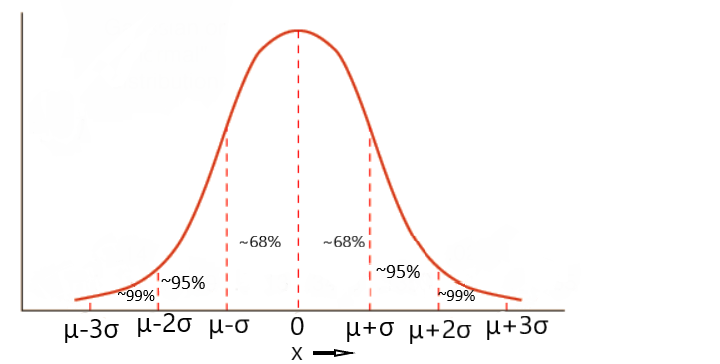

Gaussian distribution follows a bell-shaped curve and hence generally known as a bell curve.

Let us consider a random variable ‘X’ such that ‘X’ belongs to Gaussian distribution.

X∈G(µ,σ)

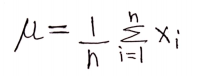

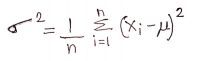

The mean is given as

The variance is given as

The Standard deviation σ=√variance

Now we look onto the empirical formula in Gaussian distribution.

The first empirical formula is given as

P(µ-σ≤X≤µ+σ)≈68%.

i.e.,68% of the total distribution will be present in the first standard deviation range.

The second empirical formula is given as

P(µ-2σ≤X≤µ+2σ)≈95%.

This means that 95% of the total distribution will be present in the second standard deviation range.

The third empirical formula is given as

P(µ-3σ≤X≤µ+3σ)≈99.7%.

This means that 99.7% of the total distribution will be present in the third standard deviation range.

Now we look onto what is called as log-normal distribution.

- Log-Normal Distribution

Consider a random variable ‘X’ such that it has the datapoints

X={x1,x2,x3,…..,xn)}

Then ln(X)={ln(x1),ln(x2),ln(x3),…..,ln(xn)}

We say that this random variable ‘X’ belongs to log-normal distribution if ln(X) is normally distributed and follows the Gaussian distribution.

Share and follow if you liked the content.